Blog

FICO SBSS Is Out: Why Your D&B, Experian, and Equifax Scores Now Decide Your SBA Funding

Summer is the busiest funding stretch of the year — and the SBA just rewrote the playbook. Effective March 1, 2026, the SBA sunset the FICO SBSS score for 7(a) small loans, retiring the blended score that had quietly gate kept thousands of approvals for more than a decade. Pair that with Experian Express pulling more community banks into the same underwriting pipeline and a fresh wave of Section 1071 reporting deadlines, and one reality stands out: your business credit file — not your personal one — is now doing the heavy lifting. Here is this week's industry update, plus the exact moves to tighten your D&B PAYDEX, Experian Intelliscore Plus, and Equifax Business Delinquency Score before lenders pull your profile.

This Week in Business Credit: 3 Shifts You Cannot Ignore

1) SBA sunset the FICO SBSS for 7(a) small loans. Effective March 1, 2026, the Small Business Administration retired the FICO Small Business Scoring Service (SBSS) as the prescreen for 7(a) small loans (loans of $350,000 or less). For more than a decade the SBSS — a blended score that combined your personal FICO, your D&B PAYDEX, your Experian Intelliscore Plus, and your Equifax commercial data into a single number — acted as the gate to SBA approval. With it gone, lenders are weighing the underlying bureau scores directly. That means a strong PAYDEX, Intelliscore Plus, and Equifax Business Delinquency Score now have more individual weight in your application than at any point since SBSS was introduced.

2) Experian Express brings more lenders online. Experian launched Experian Express in April 2026, the first fully self-service credentialing platform for community banks, credit unions, and smaller lenders. Translation: more of your local banks will now be pulling Experian business reports directly into their underwriting flow. If your Experian file is thin or inconsistent with D&B and Equifax, the denial happens faster than it used to.

3) Section 1071 reporting deadlines are live. The CFPB's revised Section 1071 rule, which requires lenders to collect and report small business loan application data, moved into its Tier 1 collection window on July 1, 2025, with Tier 2 lenders coming online January 1, 2026, and Tier 3 on October 1, 2026. More data in lenders' hands means tighter, more consistent underwriting — and less room for a weak bureau profile to slide through.

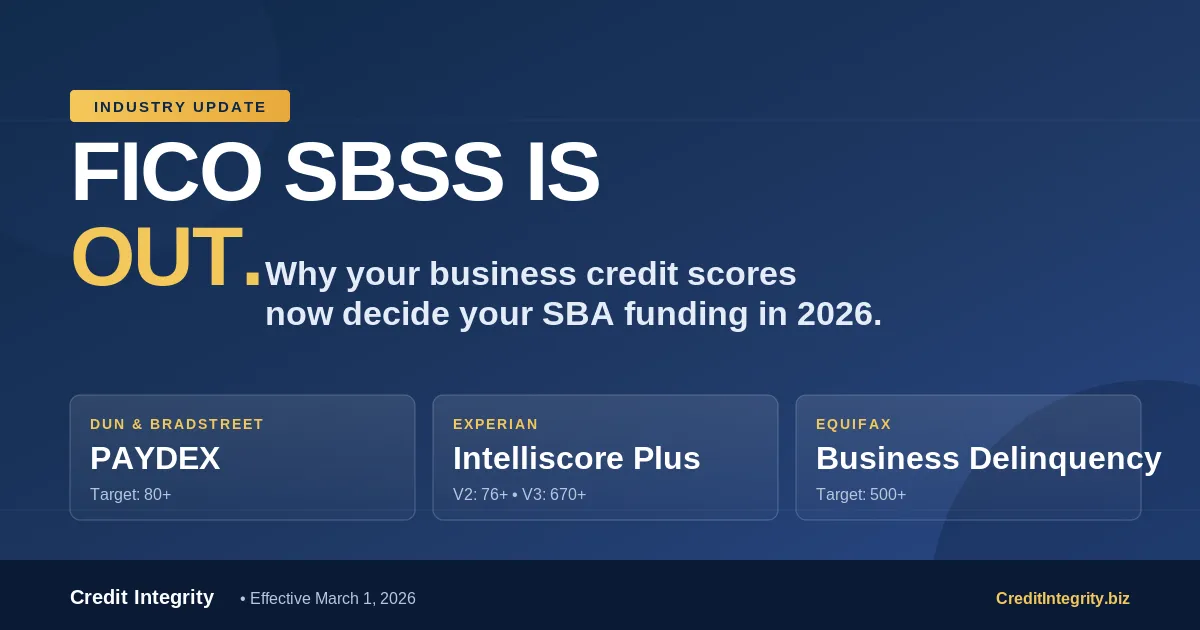

The Three Scores That Move the Needle

Every serious business credit decision in 2026 still traces back to these three bureau scores. Know them and monitor them monthly. https://nav.nkwcmr.net/xLn3n3

D&B PAYDEX

Scale: 1–100

Target: 80 or higher

What Drives It: On-time or early payments to vendors that report to D&B. Early payments push you above 80.

Experian Intelliscore Plus V2

Scale: 1–100

Target: 76 or higher

What Drives It: Payment history, credit utilization, public records, and depth of reporting tradelines.

Experian Intelliscore Plus V3

Scale: 300–850

Target: 670 or higher

What Drives It: Same signals as V2, weighted over a 24-month risk horizon. Used by fintech and larger lenders.

Equifax Business Delinquency Score

Scale: 101–662

Target: 500+ (aim for 560)

What Drives It: Predicts severe delinquency over the next 12 months. Pulls financial trades, public records, and firmographics.

5 Moves to Make Before the Summer Funding Cycle

You have roughly 8 to 10 weeks before the summer SBA and bank lending cycle hits full stride. Use them.

1.Lock in your D-U-N-S and push your PAYDEX above 80. Register a free D-U-N-S number with Dun & Bradstreet, then open 3 to 5 starter vendor tradelines with companies that report: Uline, Quill, Grainger, Shell, Speedway, Summa Office Supplies, and Crown Office Supplies are reliable. Pay invoicesearly— not just on time — because PAYDEX rewards early payments with scores above 80.

2.Pull Experian Intelliscore Plus V2 AND V3. When you request your Experian business report, specifically ask for both scale versions. Community banks still use V2; fintech lenders weight V3. You want V2 at 76+ and V3 at 670+ before your next application.

3.Keep utilization under 30%. Both Intelliscore Plus V3 and the Equifax Business Delinquency Score penalize high revolving utilization. Pay down balances aggressively in the 30 days before you apply or request a limit increase so the same balance looks smaller.

4.Dispute errors in writing with every bureau. Because business credit files are not protected under the Fair Credit Reporting Act, disputes rely on each bureau's internal process. File in writing with D&B, Experian, and Equifax separately. A single stale UCC filing or misreported tradeline can strip 30 to 40 points off your Intelliscore Plus V2.

5.Match your business identity across all three bureaus. Business name, physical address, phone number, EIN, and NAICS code must match exactly on your D&B, Experian, and Equifax files. Identity mismatches are the #1 quiet denial reason because lenders treat them as potential fraud.

Pro Tip: The Summer 2026 Lender-Ready Checklist

Run this checklist before any SBA, bank, or line-of-credit application between now and Labor Day. If you can check every box, you are positioned to qualify without pledging personal credit.

•D&B PAYDEX at 80 or higher, refreshed within the last 30 days

•Experian Intelliscore Plus V2 at 76+ and V3 at 670+

•Equifax Business Delinquency Score at 500 or higher and trending up

•Personal FICO at 680+ (still required by most SBA lenders even with SBSS retired)

•At least 5 active tradelines reporting across the three business credit bureaus

•Zero open derogatory marks — no liens, judgments, or 60+ day delinquencies

•Identical business name, address, phone, EIN, and NAICS code on all three bureau files

Want a detailed assessment and 60-day plan to hit every benchmark above?

We will pull your D&B, Experian, and Equifax files, flag what is pulling your scores down, and build you a personalized funding roadmap.

➔ Book your Consultation at https://api.profitlifter.com/widget/booking/yZmodTbncMgiOV7PtKZ7

What others are saying

Quick, Easy, and Stress-Free!

"Thanks to Credit Integrity, I secured the funding I needed to expand my business. The process was quick, easy, and stress-free!"

- Sarah M.

Equipment Financing

Finally...No More Struggling!

"I was struggling to find the right loan until I found Credit Integrity. They matched me with the perfect lender, and now my business is thriving!"

- James T.

business line of credit

Incredibly Helpful

"The team at Credit Integrity was incredibly helpful. They explained everything clearly and made the entire process so simple.

- Maria L.

SBA LOAN

Your Business Credit Profile Is Either Working For You or Against You. Let's Fix That.

Take the first step toward securing the funding your business deserves. Pre-qualify today and get matched with the perfect loan option—fast, easy, and risk-free.

Credit Infrastructure. Smart Funding. Real Results. Flexible solutions built to support your consumer credit needs, business credit growth, and funding access — helping individuals and entrepreneurs move forward with confidence at every stage.

Quick Links

Resources

Connect With Us

© Credit Integrity. 2026. All Rights Reserved.